What I read today August 14, 2020

Growth vs Value investing, Digital Media

Hi friends,

If you’re reading and enjoying the newsletter but haven’t subscribed, click on the below and it’ll arrive daily to your mailbox.

Really interesting piece to add to the Value vs Growth investing debate.

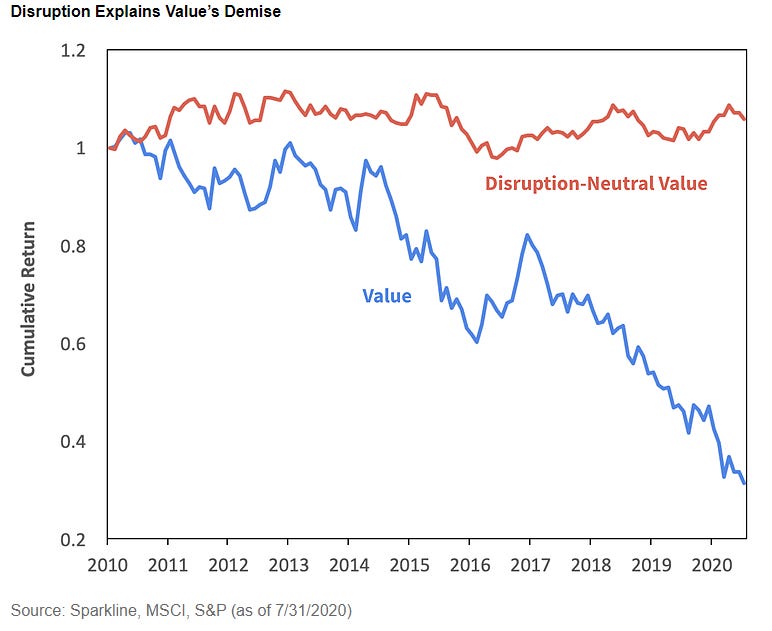

Value investing has dramatically under-performed Growth investing in recent years.

It’s significantly off its long term performance trend. If you look at what a Value portfolio consists of vs a Growth one, you would be significantly underweight stocks classified by GICS (Global Industry Classification Standard) as Information Technology, and significantly underweight the big FAANG + M stocks. Which is rough given they now make up 25% of the Russell 1000 market cap.

Interestingly though this wasn’t the only reason for portfolio difference as equal weighting industries still would lead to an unexplained 20% gap.

It turns out GICS isn’t a great way to find “disrupters” as even within industry classifications there are wide disparities in performance. Value stocks like Intel/ Cisco/ IBM are all classified as Information Technology, alongside the Visa, Microsoft, Apples of the world. The article points out that 80% of FAANG companies aren’t even in the IT category!

The researchers came up with a way to train a machine learning model to read the business description of company 10-K filings and group them on their “disruptiveness”, companies active in e-commerce, cloud, social media, SAAS etc.

Given the outperformance of FAANG+M in recent years, it’s no surprise that a disruption focused portfolio has done quite well.

A traditional value focused portfolio is not just underweight stocks in the Information Technology sector, it is also significantly underweight stocks that are disruptors. Taking them out would actually take value’s performance back to flat!

It’s a really good piece that I recommend reading as it also ties into how the narrative around value investing is changing.

When the market was dominated by large industrial concerns like railroads, factories and oil refineries, value investing was buying dollars of assets for cents. This was the Benjamin Graham “pick up a cigar butt for a couple last free puffs” approach.

Then Buffett and Munger started buying companies with low assets but great moats around their brands like Coca Cola and American Express. This was growth at a reasonable price investing, buying businesses that could reinvest their earnings back into the business at a good rate. But Buffett didn’t buy into technology at the time until his huge bet in 2016 on Apple.

The new style of “value” is now espoused by the likes of Baillie Gifford’s Scottish Mortgage Trust who’s biggest holdings are Tesla, Amazon and Tencent. I was reading the quarterly letter of a small value fund that has had good success and their focus is on growth uber alles.

The takeaway is, we need to find companies that 1) are growing quickly, 2) are capturing more value as they grow (as opposed to leaking that value away into their ecosystem), and 3) buy them at an underappreciated multiple which will (hopefully) expand over time as the company proves itself, and thus providing a tailwind to our stock performance.

The world has changed to where there are increasing returns to scale. Getting big used to be damaging but now it seems to be self-reinforcingly beneficial. It’s Marc Andreesen’s Why Software is Eating the World”. It’s being able to invest into lowering your margin rather than increasing it. Value is Growth now.

The NYT outgoing CEO thinks there won’t be a print edition in 20 years. But that’s probably fine given how digital has grown. It’s quite impressive how the NYT has built up its digital subscription service whilst also starting to monetise new streams around its IP. I’ve gone through a couple of their Podcast series recently Rabbit Hole and Nice White Parents and they’ve really carved an impressive niche building on the success they had with The Daily.

Earlier in the year I listened in to a Zoom talk by the current FT CEO where he talked about their successful transition to digital and how they had even built a consulting business around helping other businesses with their own transitions. It goes to show how core competencies of businesses change and create new opportunities, even in old school businesses like newspapers and print media.

It makes you think what other media businesses with strong digital platforms like the Daily Mail could transform into.

Other

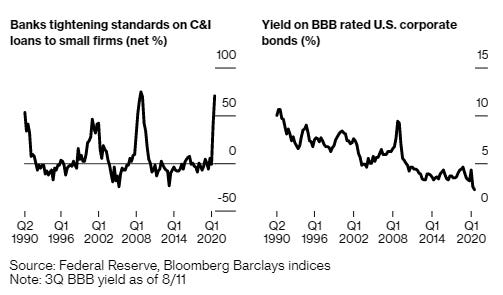

Small firms are being left behind by government stimulus. Borrowing conditions for the big firms have never been easier but access to credit via banks is tightening.

Detailed FT piece on SPACs, their evolution and why they’re suddenly so attractive to founders, investors and businesses for sale.

A detailed look at the Bicycle bubble of the late 1800s in the UK.

South Korea’s only ever Olympics Gold Boxing champion wishes he had won silver.

The history of the rice cooker. Everyone should use a rice cooker!

But there’s no shame in using rice cookers, which even in their simplest forms are an elegant solution to a tricky task. There is shame, though, in not washing your rice before you cook it. You should wash your rice.

More on rice cooking..

The offshore governor of the Central Bank of Lebanon

COVID meant no A-level exams for students, the UK went with teacher predicted grades and it’s led to some unfair adjustments.

Uber and Lyft are threatening to pull service in California after drivers have been ruled to be employees, not contractors. Will their business ever be profitable? They haven’t done too well since the IPOs.